![econlifelogotrademarkedwebsitelogo[1]](/wp-content/uploads/2024/05/econlifelogotrademarkedwebsitelogo1.png#100878)

December 20, 2023

Looking at a 1901 initial public offering and a 2023 Nippon acquisition, we could say that we are selling U.S. Steel for the second time.

Looking at a 1901 initial public offering and a 2023 Nippon acquisition, we could say that we are selling U.S. Steel for the second time.

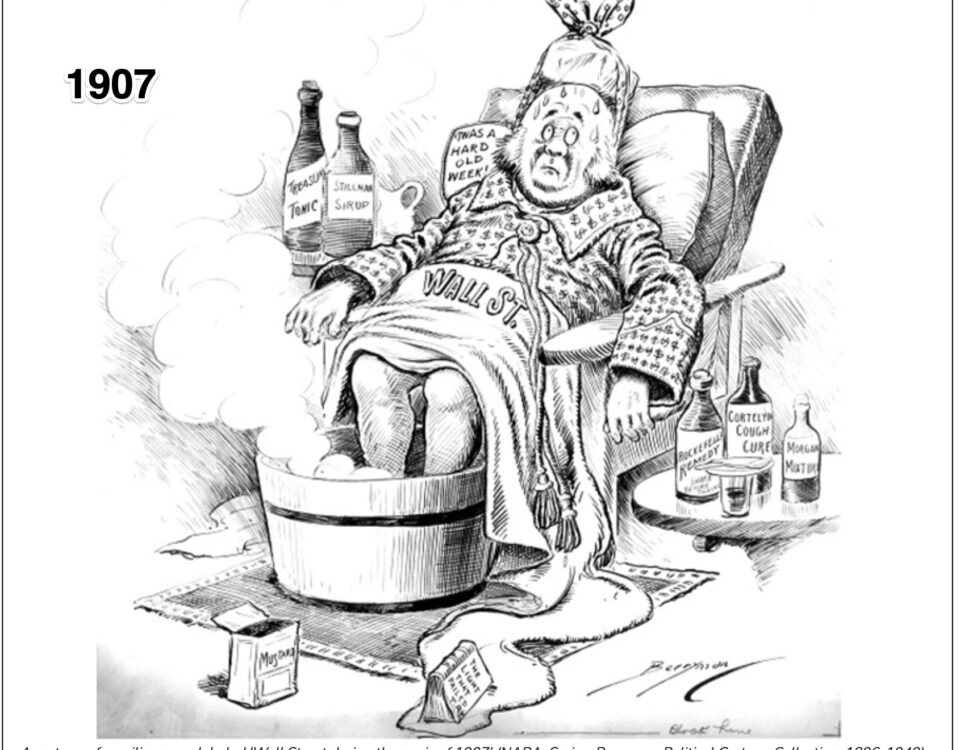

Looking at 1907 and the current turmoil in cryptocurrency markets, we could be seeing a repeat of financial history.

Debating billionaire power, we can compare J.P. Morgan in 1907 to the impact of Jeff Bezos, Richard Branson, and Elon Musk on space travel.

Rather like Apple just became the first trillion dollar corporation, in 1901 U.S. Steel took us past the billion dollar threshold.

Whether looking at a woman who needs close to $360 to pay her rent or a railroad that needs to be built, financial intermediaries are an economic necessity.

Some of the euro zone’s problems actually started with the Exxon Valdez oil spill. After the 1989 Exxon Valdez calamity, when an Alaska jury said that […]

{kind=link}

{kind=link}

{kind=link}

{kind=link}